This blog is based on a presentation made by Hanno Lustig at the SEACEN Policy Summit on 5-6 February 2026.

For much of the postwar era, the supremacy of the U.S. dollar has been treated as a permanent feature of the international monetary system. However, recent shifts in global finance suggest that we are entering a period where the fundamental equilibrium supporting this dominance is being tested. This blog invites you to examine the fiscal, institutional, and market-based mechanisms that are beginning to erode its decades-long dominance, rather than predicting that the dollar will suddenly vanish from global trade.

The Dollar Equilibrium: Safety as a Convenience Yield

To understand the potential end of dollar dominance, one must first understand what has sustained it. The system rests on a unique equilibrium: the United States supplies the world with safe, liquid assets, primarily U.S. Treasury securities, while global investors, central banks, and reserve managers absorb these assets at a premium. These assets deliver convenience yields, reflecting investors’ willingness to accept lower expected returns on Treasuries because they provide unparalleled safety and liquidity, particularly during periods of global stress.

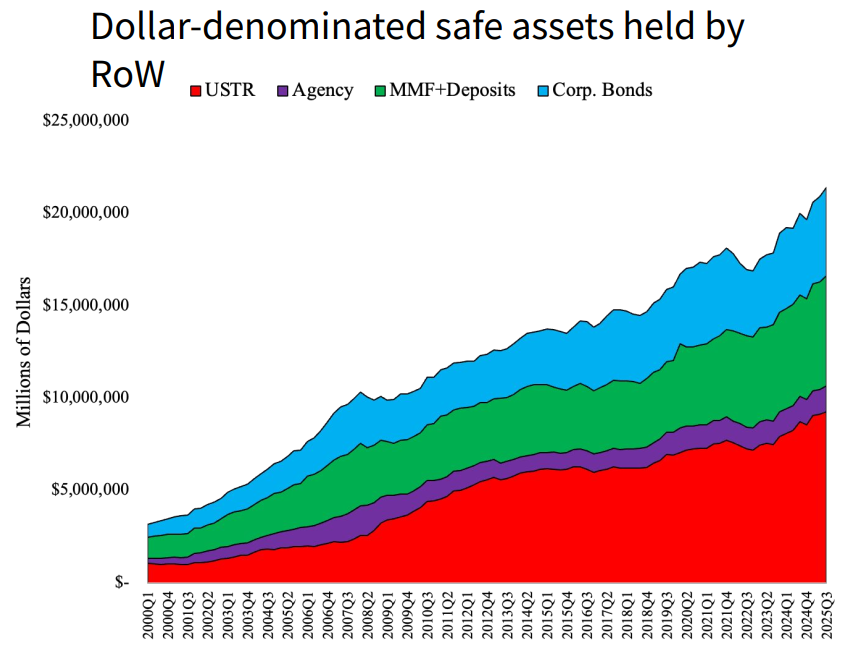

This relationship creates a structural bargain. The United States runs persistent current account deficits, essentially issuing dollar IOUs to the rest of the world. In exchange, it receives capital inflows that finance its debt at unusually favourable terms, a phenomenon often described as the exorbitant privilege. Another way to put it is, the United States is effectively “selling bonds to the rest of the world, not cars” (See Figure 1).

Figure 1: The U.S. at the centre of the international financial system, supplying over $20 trillion in safe assets.

The Pricing of Dominance: The Treasury Basis

The quantitative signature of this dominance is the Treasury basis. This metric compares the yield of an actual U.S. Treasury bond with that of a synthetic dollar bond constructed from other safe instruments. Historically, this basis was positive, indicating that the world was willing to pay a premium for the specific safety and liquidity of Treasuries. During the Global Financial Crisis of 2008, this premium spiked as investors scrambled for the world’s most trusted collateral, which created a self-reinforcing cycle: in a crisis, demand for safety rose, Treasury prices increased (yields fell), and the dollar appreciated. Thus, the global financial cycle became, in effect, a dollar cycle.

Signals of Erosion: From Premium to Discount

The most compelling evidence for the erosion of the dollar’s dominance lies in market pricing. For the first time in the post-crisis era, the marginal pricing of the Treasury’s safety services is shifting. Recent data show that Treasuries are now frequently trading at a discount rather than a premium relative to substitutes in the following 3 markets.

- Foreign Bonds: Synthetic Treasuries constructed from safe foreign government bonds (like the German Bund) with currency hedges now often offer lower yields than actual U.S. Treasuries.

- Corporate Bonds: The yield on actual Treasuries has converged with the yield of AAA-rated corporate bonds protected by credit default swaps.

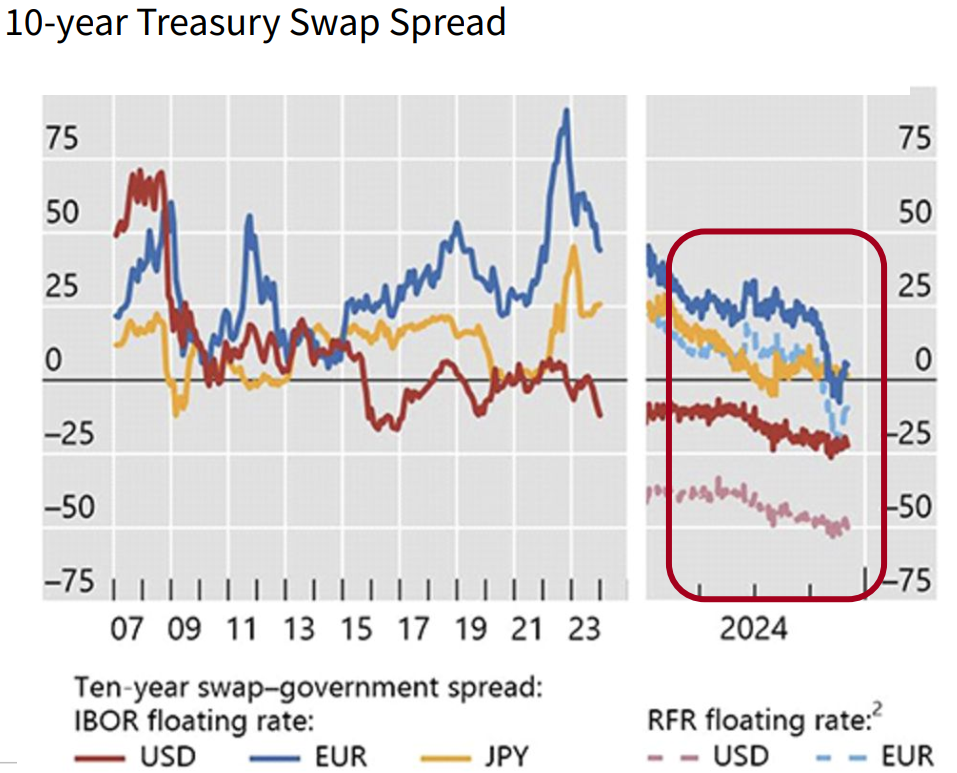

- Swaps: The swap spread has turned negative, meaning cash Treasuries sometimes offer higher yields than synthetic derivatives (See Figure 2).

Figure 2: The emergence of negative swap spreads indicates that Treasuries no longer consistently command a convenience premium.

These technical shifts signal that the world is no longer willing to warehouse ever-increasing quantities of U.S. debt at the same convenience-adjusted price. The system is beginning to reprice the risks associated with the dollar.

Triffin’s Dilemma and the Supply-Demand Paradox

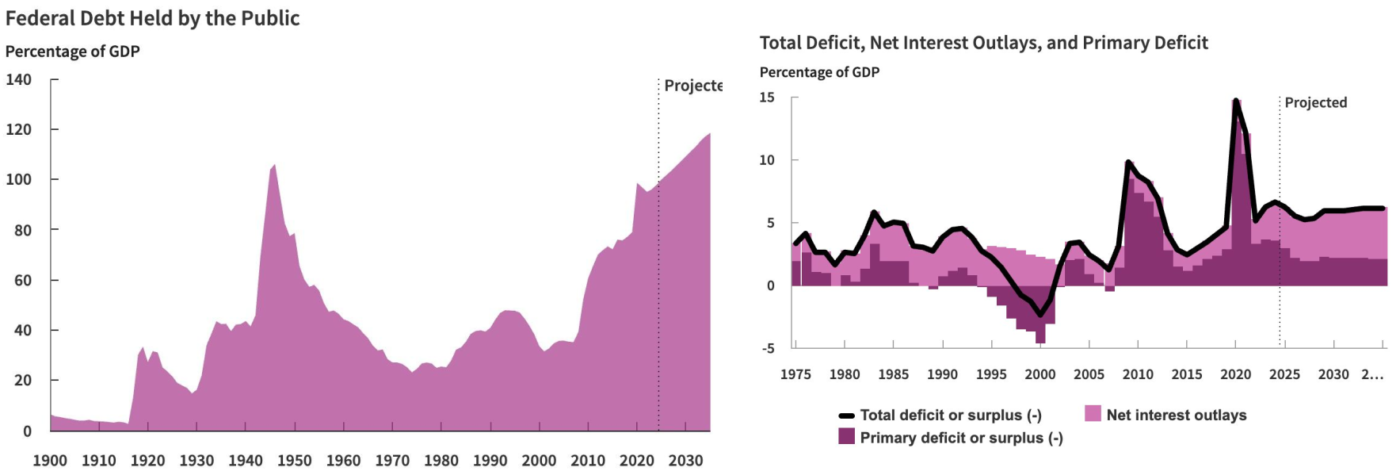

This erosion is driven by a modern version of Triffin’s Dilemma. The global economy requires a growing stock of safe dollar assets to function, but providing those assets necessitates the United States running massive fiscal deficits and expanding its public debt. As the U.S. federal debt approaches 120% of GDP and interest outlays become a primary driver of the deficit, the very safety of the “safe asset” is called into question.

When supply increases beyond the market’s natural appetite, the convenience yield must decline to attract buyers. Simultaneously, an inward shift in demand is occurring as investors reassess the reliability of U.S. markets due to political tail risks, debt-ceiling manoeuvring, and the increasing use of financial sanctions (See Figure 3).

Figure 3: The unsustainable fiscal trajectory of the United States, with debt held by the public projected to rise significantly.

Shattering the Flight-to-Safety Mechanism

The true test of dollar dominance is how the system behaves under extreme stress. Historically, a crisis meant a flight to safety into the dollar. However, two recent episodes suggest this mechanism is broken.

In March 2020 (the first episode), the onset of the pandemic triggered a “dash for cash”, with the foreign sector not serving as a stabilising buyer. Instead, the Treasury market faced selling pressure as investors sought immediate liquidity. The system cleared only because the Federal Reserve intervened as the “dealer of last resort”, absorbing a substantial share of the supply to prevent a market breakdown.

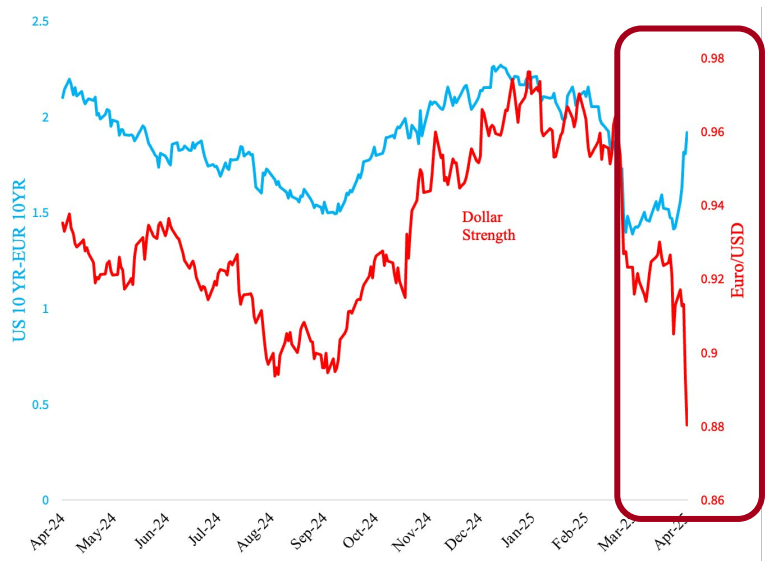

More telling is the second episode, “Liberation Day,” in April 2025. During a period of heightened market volatility (a VIX spike), U.S. long-term interest rates rose while the dollar depreciated by 3.6%. This is the exact opposite of the classic flight-to-safety pattern. It indicates that the market treated Treasuries not as a safe haven but as an asset that required a yield concession to hold (See Figure 4).

Figure 4: In April 2025, the dollar depreciated as yields increased, signalling a “flight from Treasurys”.

Policy Implications for a Multipolar World

For central banks and policy makers, particularly in Asia, the end of this specific dollar equilibrium has first-order implications. If the dollar begins to trade like a standard currency, traditional reserve-management strategies must change.

A world with a less dominant dollar could offer some benefits, such as reduced currency mismatch in emerging markets. If borrowing in dollars becomes less attractive, the mechanical tightening of financial conditions caused by a strengthening dollar during crises might dampen. However, a fragmented or multipolar system also carries risks: higher hedging costs, reduced market depth, and greater volatility in the absence of a singular safe-asset anchor.

Conclusion

The “End of Dollar Dominance” is likely be a gradual repricing of the global safe-asset equilibrium. The evidence suggests that the special “convenience yield” that has underpinned the U.S. dollar for decades is fading. As the United States struggles with an unsustainable fiscal path and the flight-to-safety mechanism becomes increasingly state-dependent, the international monetary system is moving toward an uncertain, multipolar future. For the global policy community, the challenge is no longer merely managing the dollar cycle but preparing for a world in which the dollar no longer provides the insurance it once did.