In February 2021, the price of Bitcoin skyrocketed to over US$58,000 after Elon Musk’s Tesla said it had bought up US$1.5 billion of the cryptocurrency. One major Bitcoin investor said he saw the price rising to US$100,000 by the end of the year. The meteoric rise in the price of Bitcoin is more than 1,000 per cent since March 2020. In 2017, we saw a similar bull run in the price of Bitcoin. But the Bitcoin boom bust dramatically in early 2018, resulting in the dissipation of a gigantic portion of the market capitalisation of major cryptocurrencies.

The consensus is that the 2017 Bitcoin bull run was largely fuelled by speculation and retail investors’ fear of missing out (FOMO). So, what has changed since then? Nothing really!

There are three factors currently driving the price of Bitcoin, namely:

- Fear of inflation and the inflation hedge

- Institutional investors and FOMO

- Halving and scarcity

Fear of Inflation and the Inflation Hedge

Bitcoin has been around for more than a decade now since it was created and introduced to the world by Satoshi Nakamoto, the pseudonymous person or persons who developed it and published the white paper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System‘. Bitcoin is largely viewed by its proponents as an inflation hedge because of its limited supply, which is not influenced by its price, and because of its perceived relative attractiveness when real yields head to zero or lower. In addition, Bitcoin has a finite and fixed supply of 21 million.

Bitcoin, these proponents allege, is also a hedge against the pernicious debasement of currency through a loss of trust. Traditionally, inflation moves in tandem with the strength of the local economy. But it can be triggered by currency weakness, which raises the prices of imported goods. This is usually corrected when the central bank raises interest rates to combat rising inflation, which increases the attractiveness of the currency compared to others.

The infusion of cash into the financial system in response to COVID-19 has renewed concerns that inflation could surge. This view is in line with Milton Friedman who said more than once that “inflation is always and everywhere a monetary phenomenon”. If you subscribe to this view, then when you look at central banks’ balance sheets exploding right now, you are bound to conclude that there is going to be inflation. This may be partially true, as market gauges do show inflation coming back: 30-year US Treasury yields topped 2 per cent recently for the first time in a year; UK government bonds slid, and oil rallied. The key message here from the market is that a post-COVID-19 economic recovery, assisted by massive fiscal and monetary stimulus, will fuel inflation but this does not mean will get beyond targeted levels of 2 per cent inflation.

Obviously, we should not kid ourselves about the pains of inflation. The worry is indeed justified. The amount of liquidity in the monetary system is alarmingly high, so the snap-back will likely be stronger, thereby giving rise to inflationary concerns. The question is what will happen when economic stimulus runs out or the time does come to pull back. Despite policy makers’ best effort for a carefully orchestrated rollback of economic stimulus, this may be painful. The experiences of the 2013 taper tantrum that sent markets into a tailspin is testimony to the challenges ahead post-COVID-19.

To hedge against inflation, investors are searching for assets that either maintain value or appreciate in value. The fundamental question that needs to be answered is whether Bitcoin serves as a good store-of-value, and consequently a good hedge against inflation?

Institutional Investors and FOMO

It is difficult to discern the motivation for the current ‘race to the moon’ in the price of Bitcoin. Whatever the motivation, the record-breaking rally has led to a surge in retail investment interest in the cryptocurrency market. Some of the major crypto exchanges have seen a spike in activity pointing to increased retail participation.

In January, the total market value of all cryptocurrencies surpassed US$1 trillion for the first time driven primarily by the meteoric performance of Bitcoin. But it is not just Bitcoin that is surging. Altcoins, which are digital tokens that came after Bitcoin, are also rallying. This is seen through the increase in the signing up of new accounts and trading volumes on crypto exchanges such as Coinbase and Binance and online retail platforms including Revolut and eToro that are more targeted to retail investors. EToro, for example, had 61 per cent more unique Bitcoin holders in January than it did a year earlier, and 49 per cent more unique holders of ether. Revolut says Bitcoin was the most popular digital currency on its platform, and it signed up 300,000 new cryptocurrency customers over the last 30 days as Bitcoin rallied to fresh highs. Prices of altcoins, such as ether, litecoin and Bitcoin cash, have also risen dramatically so far this year. They often rally in times of strength in Bitcoin — for example, ether in January climbed past US$1,000, for the first time since February 2018.

Crypto analysts seem to suggest that the 2021 Bitcoin bull is different from the 2017 bubble that saw its price soar close to US$20,000 before collapsing to as low as US$3,000 in early 2018. They argue that the main difference is the interest and participation of institutional investors. Since 2020, we have seen a steady stream of institutional investors making public pronouncements relating to the activities and status in the cryptocurrency and virtual assets space. Notable investors such as Paul Tudor Jones and Stanley Druckenmiller invested in Bitcoin while punting its merits as an inflation hedge. The UK asset management firm Ruffer is reported to have added £550 million (US$747 million) of Bitcoin to its portfolio. Large financial companies like PayPal and Fidelity have also made moves in the cryptocurrency space while the likes of Square and MicroStrategy have used their own balance sheets to buy Bitcoin. MicroStrategy, the first corporation to directly purchase Bitcoin, now owns 70,784 Bitcoin, worth more than US$3.5 billion. Its Chairman and CEO, Michael Saylor, has long advocated Bitcoin, viewing the cryptocurrency as a hedge against a devaluation of the US dollar.

News of Tesla’s disclosure in its filing with the US Securities and Exchange Commission in January that it had bought US$1.5 billion of Bitcoin helped to fuel the surge in the cryptocurrency price. The company said it had “updated our investment policy to provide us with more flexibility to further diversify and maximise returns (p. 23)” to allow it to invest cash reserve in “alternative reserve assets including digital assets (p. 23)”. It said that since the decision was approved by its audit committee it had “invested an aggregate $1.50 billion in Bitcoin under this policy and may acquire and hold digital assets from time to time or long term (p. 23)”. In keeping with the current trend of using Twitter, Elon Musk said Tesla’s decision to buy US$1.5 billion in Bitcoin was a company decision not driven by him. On Twitter, Musk said “Tesla’s action is not directly reflective of my opinion. Having some Bitcoin, which is simply a less dumb form of liquidity than cash, is adventurous enough for an S&P 500 company”. In another tweet, he added “…when fiat [government-issued] currency has negative real interest, only a fool wouldn’t look elsewhere. Bitcoin is almost as bs as fiat money. The key word is ‘almost’ “.

The question is whether the participation of institutional investors means that Bitcoin is now mainstream. As noted earlier, many crypto investors see Bitcoin as a hedge against inflation. It is, according to them, akin to ‘digital gold’, a potential safe haven asset. Strategists at JPMorgan recently gave a lofty long-term price target of US$146,000 for Bitcoin, claiming it is starting to compete with gold as an ‘alternative’ currency. But the risk of an abrupt reversal is high, and truthfully retail investors are likely to ignore volatility.

Based on the above, it seems the recent gains in altcoins are attributable to retail participation, and the surge in Bitcoin is driven by institutional investors. In 2017, one of the concerns arising out of the Bitcoin bubble was the implication for financial stability. In 2017, retail investors were using leverage to invest in Bitcoin. They used their credit cards to open accounts on crypto exchanges and acquire cryptocurrencies. The fact that there are signs of a sharp rise in demand from retail investors may have significant implications for the latest crypto market cycle, given the role that retail speculation played in the 2017 bubble.

As noted earlier, there have been ‘some signs that retail interest has also increased sharply’ based on rising volumes on platforms like PayPal and Square’s Cash App. PayPal last year launched a feature in the US that lets its users invest in cryptocurrencies. The company plans to offer crypto shopping across its massive network of retailers later this year. The move is widely seen as a step toward mainstream adoption of crypto in activities like payments. While this might seem well intended, we should not dismiss retail investments in Bitcoin as simply individuals stuck at home due to the ongoing COVID-19 global pandemic using their stimulus checks to acquire Bitcoins. Recent events relating to GameStop and r/wallstreetbets point to young people using their student loans to play the stock market. Such investment decisions have wider implications for these individuals’ financial well-being and the financial health of our societies.

We conclude that in 2021, when compared to 2017, the regulatory landscape is slightly different. Today, there is a little more certainty in terms of regulations, and this will likely help to attract more institutional investors. On a somewhat related note, most central banks around the world are currently exploring Central Bank Digital Currencies (CBDCs). CBDCs are not Bitcoins or cryptocurrencies, because the presence of the central banks or central authority does not make them decentralised like Bitcoin. In addition, with CBDC, the central bank will likely retain core control over supply, and rules will likely remain in the hands of the banks or governments. Developments relating to CBDC show the government’s recognition of the necessity for a more advanced payment system than paper cash provides. This trend further lends merit to the concept of cryptocurrencies and their convenience in general, and the fact that regulators and policymakers are much more comfortable and open to the merits of Bitcoins, stablecoins and virtual assets than they were in 2017.

Halving and scarcity

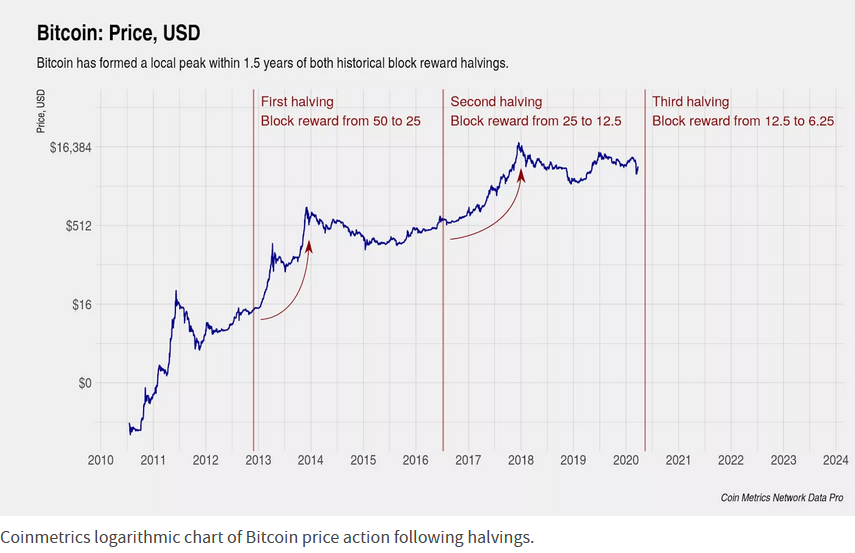

We noted earlier that Bitcoin has a finite and fixed supply of 21 million. This verifiable finite limit can be best understood through an explanation of the mechanism known as Halving. For every 210,000 blocks of Bitcoins that are mined, or about every four years, the reward given to miners for processing Bitcoin transactions is reduced in half. Built into Bitcoin is a synthetic form of inflation in that miners are rewarded with Bitcoins and this adds new Bitcoin into circulation. The rate of this inflation is cut in half every four years and this will continue until all 21 million Bitcoin are released to the market. Currently, there are 18.5 million Bitcoins in circulation, or about 88.4 per cent of Bitcoin’s total supply. As Bitcoin has a finite amount and its supply is reduced over time, the price of Bitcoin can be kept ‘stable’ and deflationary by reducing the overall supply –- this is why Bitcoin halving exists. Halving reduces the supply of Bitcoin, and thus based on scarcity, it also contributes to driving up the price of Bitcoin.

The first halving, which occurred in November 2012, saw a price increase from about US$12 to nearly US$1,150 within a year. The second Bitcoin halving occurred in July 2016. The price at that halving was about US$650, and by 17 December 2017, Bitcoin’s price had soared to just under US$20,000. The price then fell over the course of a year from this peak down to around US$3,200, a price nearly 400 per cent higher than Its pre-halving price. Bitcoin’s third having just occurred on 11 May 2020 and its price has since increased astronomically.

Onchain statistics show 78 per cent of the circulating Bitcoin supply is illiquid and barely accessible, according to Glassnode research. Data indicate that the analysts have classified 14.5 million Bitcoin as illiquid, and only 4.2 million Bitcoin are in constant circulation for buying and selling. This suggests that a large portion of Bitcoins are hoarded, and consequently, it is possible that the current uptrend in crypto asset value has been fuelled by liquidity issues.

As noted above, a number of large regulated financial institutions and institutional investors including well-known hedge fund managers have entered the Bitcoin market. They are acquiring Bitcoin in significantly large quantities. In some instances, Bitcoin acquisitions are held as treasury reserves. According to research from Glassnode, the rising illiquidity suggests “the current bull run has been (partly) driven by this emerging Bitcoin liquidity crisis”. Glassnode concluded that the amount of liquid and illiquid Bitcoin in circulation had a “clear relationship with the BTC market.” Data show that since 2017, the illiquid holdings of Bitcoin have swelled more so than the issued Bitcoin stemming from Bitcoin miners. This pattern was observed during the crypto asset run-up in 2017 as well, as detailed by Onchain researchers.

Summary and conclusion

What has changed since 2017?

Nothing!

Bitcoin has been and will always be extremely volatile. Recently the price of Bitcoin climbed to a record high of US$58,042, bringing its year-to-date gain to over 100 per cent and the market capitalisation to US$1 trillion. In no time, the price tumbled as much as 17 per cent to below US$48,000. Volatility is a feature of Bitcoin, and this volatility brings into question it merits as a store of value. Prudent financial management would suggest that individuals should only invest what they can reasonably and affordably lose in Bitcoin. Otherwise, they should steer clear of the cryptocurrency because of its wild swings.

Bitcoin was inefficient and speculative in 2017, and it still is in 2021. Replying on Twitter to Peter Schiff, a stockbroker and gold investor, Musk said: “Money is just data that allows us to avoid the inconvenience of barter. That data, like all data, is subject to latency and error. The system will evolve to that which minimises both. That said, Bitcoin and ethereum [another cryptocurrency] do seem high”.

On Monday, 22 February 2021, Janet Yellen, US Treasury Secretary and former Federal Reserve Chair warned that Bitcoin is an “extremely inefficient” way to conduct monetary transactions and emphasised its use in illicit activity.

She also sounded the alarm about Bitcoin’s impact on the environment. The token’s wild surge has reminded some critics of the sheer level of electricity required to produce new coins. So-called miners run high-powered machines that compete to solve complex math puzzles in order to make a transaction go through. Bitcoin’s network consumes more electricity than Pakistan, according to an online tool from researchers at Cambridge University. Yellen also warned about the risks for retail investors buying Bitcoin. She noted that it is a highly speculative asset, and people should be aware it can be extremely volatile and the potential losses that investors can suffer.

Mark is a Senior Financial Sector Specialist in the Financial Stability, Supervision and Payments pillar at the SEACEN Centre.