This blog is based on a presentation made by Jeffrey Frankel at the SEACEN Policy Summit 2026: The Future of the International Monetary System and the Role of Asia (5– 6February 2026).

The Dollar’s Legacy and Its “Exorbitant Privilege”

The U.S. dollar supplanted the British pound as the dominant international currency in the 20th century. The transition was underpinned by the country’s growing economic strength and its commitment to supply a safe and liquid global asset.

The dominance of the dollar gave the U.S. what French finance minister Valéry Giscard d’Estaing (1960) famously called an “exorbitant privilege”, namely the ability to finance deficits and earn seigniorage by issuing the global reserve currency. For decades, the world accepted this as the necessary price of a stable and open U.S.-led global economic and financial system.

Cracks in the System: Decline in Dollar Share

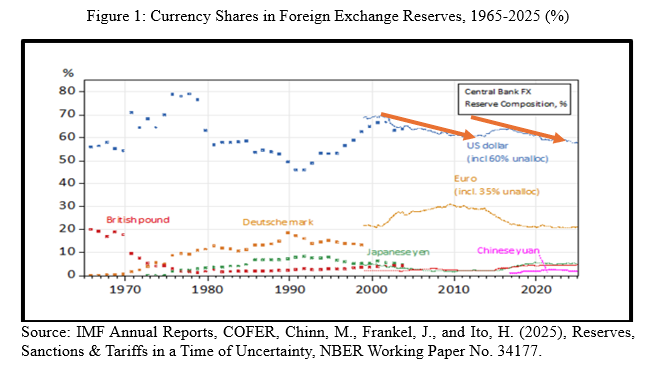

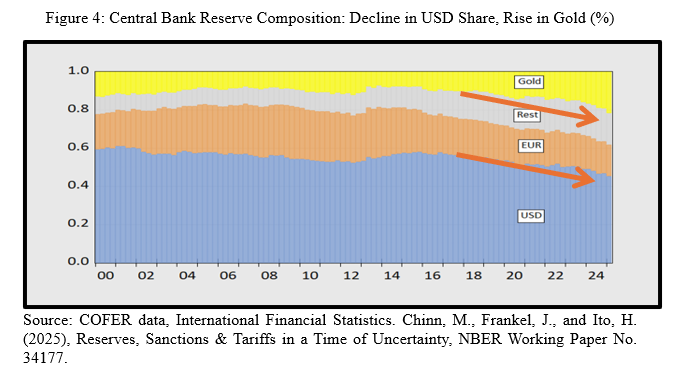

Yet in recent decades, the relative decline of the U.S. economy is eroding the dollar’s supremacy. Its share in global foreign exchange reserves fell gradually from around 70% in 2001 to just under 57% in 2025. While the dollar still remains the dominant reserve currency by a wide margin, this downward trend has accelerated in recent years due to both U.S. specific and global economic and geopolitical factors.

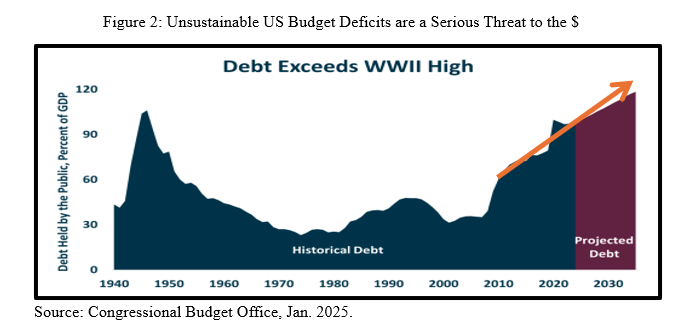

One key factor is the misuse of the dollar’s exorbitant privileged status. Rising concerns about U.S. fiscal policy, especially soaring deficits, money financing, and risk of default, led some to question the long-term sustainability of dollar assets. Moreover, the frequent and excessive use of financial sanctions by the U.S. without multilateral backing has led many countries to reassess the currency composition of their reserves.

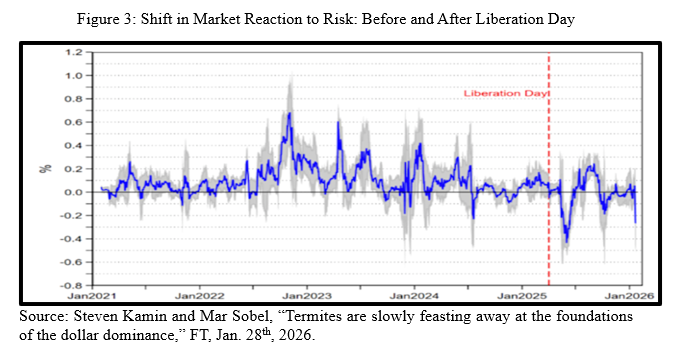

According to recent research by Chinn, Frankel, and Ito (2025), bilateral financial sanctions and trade policy uncertainty have significant negative impacts on the US dollar holdings of 50 central banks over the period 1990–2022. The weakening of the safe haven status was illustrated on “Liberation Day,” April 2, 2025, when markets faced with heightened global risk shifted out of the dollar, in sharp contrast to the Global Financial Crisis which saw the greenback rise despite the crisis originating in the U.S.

More broadly, many central bank reserves managers are gradually reducing their exposure to the US dollar while increasing allocations to other reserve assets, especially gold.

From Hegemony to Multipolarity?

Given the dollar’s decline, could we be heading toward a multiplex or multi-currency system? Such transition is both plausible and already unfolding. While the euro and Chinese renminbi are often cited as potential challengers, they lack the deep, liquid, and open financial markets required for global reserve currency status. Even so, modest shifts are occurring. Some central banks are incrementally allocating reserves to RMB and gold (as shown by Arslanalp, Eichengreen & Simpson-Bell (2023)), signalling their dissatisfaction with the dollar despite the lack of a viable alternative currency.

There is a fundamental trade-off at the heart of the international monetary system. A dominant international currency like the dollar offers low transaction costs and global stability but entails the risk of significant abuse by the issuing country. A multi-currency system, while more complex, could impose discipline by making it harder for any one country to exploit its position unchecked. That seems to be the direction the system is evolving toward, albeit only slowly.

The Role of Digital and Regional Currencies

Adding further complexity to the monetary landscape is the rise of digital currencies. Skepticism toward cryptocurrencies persists, with critics viewing them largely as vehicles for speculation or regulatory evasion. In contrast, central bank digital currencies (CBDCs) may offer more credible innovations by reinforcing the role of central banks in the financial system.

Regional currencies too are gaining traction. Asia, for example, is witnessing the growing use of the Japanese yen and the Singapore dollar in regional trade. Yet it is China’s RMB, the currency of the region’s economic heavyweight, that garners the most attention. However, its rise has been hampered by Beijing’s reluctance to fully liberalize capital controls.

An Unpredictable Hegemon

But U.S. behaviour in recent years has gone beyond the abuse of its exorbitant privilege as traditionally understood. In fact, the US has undermined the very international system it helped build after World War II. The postwar order of multilateral cooperation, free trade, freedom of the seas, world health cooperation, 80 years of relative peace, and much more is fraying due to America’s own retreat from its leadership role.

Through erratic tariff policies, attacks on the independence of the Federal Reserve, flirting with government default or with taxing foreign-held debt, quitting international institutions, gratuitous ruptures with allies, and threatening to violate territorial sovereignty of another country, the U.S. administrations has severely disrupted the global economic and financial system. The erosion of the dollar’s global status due to economic and financial forces is thus compounded by institutional weakness and geopolitical uncertainty.

The Path Ahead

So, what lies ahead for the international monetary system? The continued dollar dominance is likely but not guaranteed in the medium term. Its dominance ultimately rests on the credibility and predictability of U.S. policy, strong US institutions, deep, safe and liquid American financial markets, and the absence of a viable alternative. If these conditions erode further, the transition to a more balanced, multipolar arrangement will accelerate.

In the meantime, a cautious evolution already appears underway, evident in modest reserve diversification into gold and alternative currencies, growing interest in CBDCs, and a latent desire for reform. Whether this path eventually leads to greater stability and predictability or to fragmentation, uncertainty, and volatility, remains to be seen.

References:

Arslanalp, S., Eichengreen, B., & Simpson-Bell, C. (2023) “Gold as International Reserves: A Barbarous Relic No More?” Journal of International Economics.

Chinn, M., Frankel, J., and Ito, H. (2025). “Reserves, Sanctions & Tariffs in a Time of Uncertainty.” National Bureau of Economic Research Working Paper No. 34177.

Kamin, S. and Sobel, M. (2026, January 28). “Termites are slowly feasting away at the foundations of the dollar’s dominance.” Financial Times. www.ft.com/content/093332b0-1502-4668-b4e1-32b7e30cb172.