Introduction

Since the Asian financial crisis of 1997-98, emerging and developing economies (EMDEs) in Asia have strengthened their resilience to external financial shocks by upgrading macroeconomic management frameworks, reforming financial sectors, accumulating FX reserves, making exchange rates more flexible, avoiding excessive short-term dollar inflows, and introducing a regional financial safety net and surveillance process.

As a result, Asian EMDEs were able to weather the global financial crisis of 2008-09, the taper tantrum of 2013, and the pandemic of 2020-21 relatively well. However, given the recent emergence of daunting common risks, such as spillovers from U.S. policy uncertainty, financial digitalization, trade frictions, and geopolitical fragmentation, Asia should make further efforts to enhance national policy frameworks and regional monetary and financial cooperation.

Progress on Regional Monetary and Financial Cooperation

In the aftermath of the Asian financial crisis, Asian economies have made notable progress in regional monetary and financial cooperation. The progress is most visible in in three areas, namely regional financial safety net and economic surveillance, local-currency (LCY) bond market development, and LCY payment connectivity.

First, the most significant is the development of the Chiang Mai Initiative Multilateralization (CMIM), which is the regional financial safety net for the ASEAN+3 region[1]. With a total size of US$240 billion, the CMIM provides a crisis response facility called the Stability Facility, a crisis prevention facility called the Precautionary Line, and a recently introduced facility called the Rapid Financing Facility (RFF) designed to quickly respond to sudden shocks such as pandemics and natural disasters.

Over time, the CMIM has reduced links with IMF programs through a gradual increase in the IMF-delinked portion (IDLP), from 10 percent initially to 40 percent today. Discussions are ongoing on transforming the CMIM from a network of multilateral currency swap lines into a paid-in capital structure like the IMF.

ASEAN+3 authorities have also introduced a regional economic surveillance mechanism by establishing the ASEAN+3 Macroeconomic Research Office (AMRO). AMRO conducts national and regional economic surveillance, identifies areas of weaknesses and vulnerabilities for each member economy, and provides policy recommendations to address them.

Second, ASEAN+3 economies have pursued policies to develop LCY long-term bond markets under the Asian Bond Markets Initiative. Expanding LCY bond markets helps reduce excessive reliance on domestic banks and short-term foreign-currency loans, thereby mitigating the double mismatch problem. With the banking sector augmented by the LCY bond market, Asian economies have become more resilient to external and domestic shocks. Other SEACEN member economies may adopt a similar approach to promote LCY bond markets to support their economic development.

Third, Asian economies led by ASEAN member states have been linking their LCY payment systems. Under the Regional Payment Connectivity initiative and the LCY Settlement Framework, ASEAN members have bilaterally linked domestic QR code payment services of their fast payment systems to facilitate real-time cross-border payments. These efforts promote faster, cheaper, more transparent, and more inclusive cross-border payments. To date, the QR code payment services of most ASEAN economies are connected bilaterally with each other and such connections are expanding to Hong Kong, India, Japan, and others.

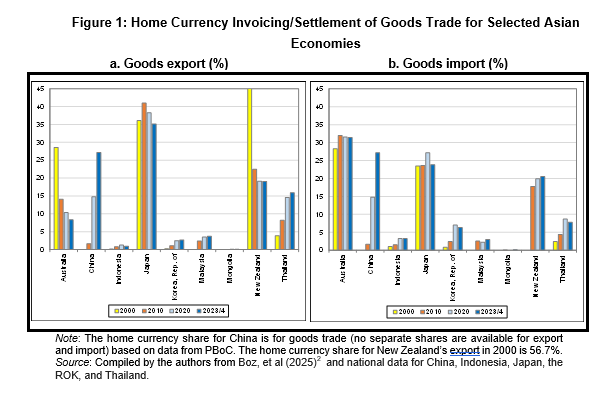

ASEAN’s LCY Settlement Framework has contributed to the growth of home-currency invoicing and settlement in goods trade. Figure 1 demonstrates that home-currency use remains generally low in emerging economies compared to advanced economies. Nonetheless, China’s home-currency share has risen rapidly over time, followed by Thailand, Malaysia, and Indonesia. The Regional Payment Connectivity initiative is expected to further increase home-currency use in Asia’s cross-border transactions.

[1] Comprising ASEAN’s 10 members plus China, Hong Kong, Japan, and the Rep. of Korea (ROK).

Toward A More Effective Regional Financial Safety Net

While Asian economies have made a lot of progress on regional monetary and financial cooperation, there is substantial scope for further progress. In particular, given the risk of more volatile capital flows in an era of policy uncertainty, digitalization, and fragmentation, Asian monetary authorities need to work closely together to strengthen the regional financial safety net.

More specifically, the ASEAN+3 authorities could:

- Increase CMIM financing capacity for member economies;

- Raise the IDLP over time, eventually to 100%;

- Transform the CMIM contribution modality to a paid-in capital or quota-based structure a la IMF;

- Enhance CMIM’s flexibility to quickly respond to shocks such as rapid cross-border digital transactions that affect balance of payments;

- Upgrade AMRO’s function as a permanent surveillance center of all aspects of the CMIM and as technical secretariat

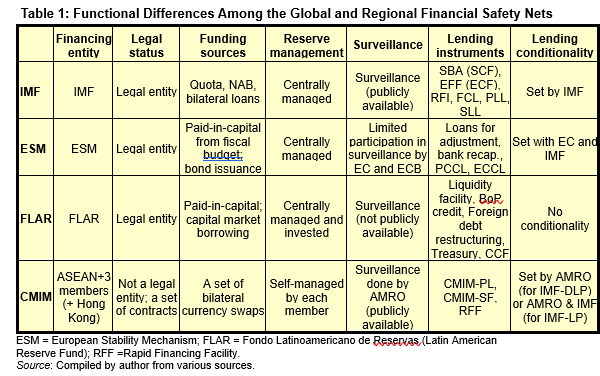

- Integrate CMIM and AMRO into a single legal institution (Table 1). In Table 1, the CMIM has no legal status unlike the IMF or other regional financing arrangements;

- Widen the membership of the CMIM/AMRO to include Australia, New Zealand, and other SEACEN members;

- Form an Asian Troika involving the IMF, CMIM/AMRO, and ADB for the management of a large-scale financial crisis.

In order to raise the CMIM’s IDLP ultimately to 100%, the Asian region needs to develop a culture that allows frank discussions on the weaknesses and vulnerabilities of each other and policy reforms needed to prevent crises as well as appropriate policy adjustments in the event of a crisis.

Importantly, strengthening regional financial safety nets need not come at the expense of neglecting cooperation with global institutions. AMRO and CMIM should work hand in hand with the IMF to safeguard regional financial stability. Close cooperation is especially vital for tackling large-scale crises which require substantial amounts of financing.

Conclusion

Facing significant new common challenges such as U.S. policy uncertainty, trade frictions, and geopolitical fragmentation, Asia needs to reinforce regional monetary and financial cooperation to sustain growth and financial stability. The rise of digital financial assets strengthens the case for deeper regional monetary and financial cooperation. The risk of cross-border digital financial spillovers dictates that Asian monetary authorities coordinate with each other. For instance, they need to regularly exchange information and harmonize divergent national regulations.

Priority areas for stronger cooperation include enhancing regional macroeconomic and financial surveillance, bolstering the effectiveness of the CMIM and AMRO ultimately integrating them into a single international institution with legal status, deepening local-currency (LCY) bond markets, promoting the use of LCYs in trade and investment, including through LCY stablecoins and central bank digital currencies, and stepping up regional payment connectivity while harmonizing regulatory frameworks on cross-border payments.

For SEACEN member central banks, the priorities translate into practical actions such as intensifying data sharing and policy dialogue, supporting interoperability of fast payment systems, developing LCY financial markets, enhancing supervisory and regulatory coordination on digital finance, and contributing actively to regional surveillance and crisis-preparedness mechanisms. Through sustained collaboration, SEACEN members can play an important role in shaping a more resilient and inclusive regional financial architecture.