In this Suara SEACEN article, we show that global output growth slows down during pandemics, and global growth in the post-pandemic period is slightly lower than the pre-pandemic period. This article argues that public health must remain the top priority; and fiscal stimulus that will cushion the severe impacts of the pandemic must play dominant roles in policy responses.

The ongoing COVID-19 pandemic, which began in January 2020, has led to unprecedented global responses with the aim of slowing down the virus transmission. Policy responses involving contact tracing, early detection to through testing, social distancing and public health information are integral measures intended to slow down the rate of infection. But given the voracity of the virus, due mainly to the lack of complete information on the new virus including its methods of transmissions as well as available vaccine and treatment, tougher measures are needed to reduce the rate of human-to-human transmission and local community outbreaks. Subsequently, governments have imposed travel bans, quarantines, city-wide lock downs and movement controls. These tougher measures are intended to flatten the curve of infection so as not to overwhelm and paralyse the health care system. These measures will also buy time until more is known about the virus, specifically about its transmission and treatment.

These tougher measures in controlling the virus have their downside consequences. Specifically, nation-, region- and city-wide lock downs translate into significant output contractions due to demand and supply-side effects. On the demand-side, consumer demand for goods and most services are substantially curtailed. This translates into loss of revenues and income from businesses and service providers. For instance, the travel ban and quarantines led to almost all passenger airlines operating below 10 per cent of their capacity (although cargo services remain strong). On the supply-side, the manufacturing sector is the hardest hit given tougher measures to combat the spread of the virus. Primary indicators such as electricity load, unemployment benefit claims, purchasing manager indices and even atmospheric concentrations of nitrogen oxide have all pointed to sharp dips or spikes since the start of containment measures. Consequently, the head of the International Monetary Fund has said that the global economy may undergo a recession, while the Asian Development Bank expects regional growth to slow sharply to 2.2 per cent in 2020.

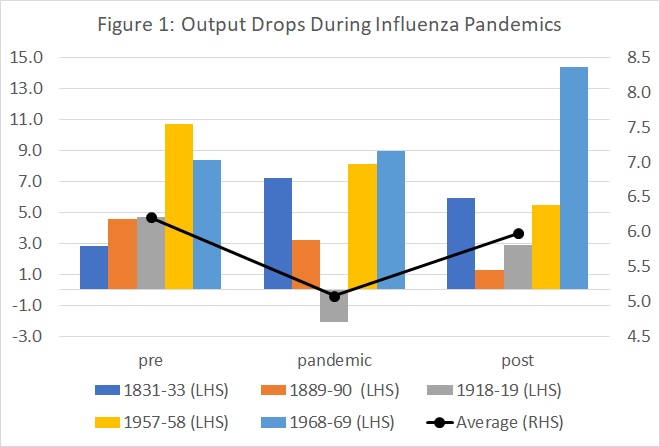

With the ongoing uncertainty on the how the COVID-19 pandemic will affect output, perhaps past episodes of pandemics may shed light on the magnitude of output drops and growth slowdowns the present pandemic may impart on the global economy. Potter (2001) discussed various influenza pandemic episodes from the 18th to the 20th centuries.[1] But to have insights on how output behaves before, during and after pandemics, focusing on pandemics from 1820’s onwards is more insightful for two reasons. First, the industrial revolution took off between 1820 to 1840. Hence, both the agricultural and manufacturing sectors were relatively developed in some economies around that time. Second, the Maddison Historical Statistics have available estimated data for economic output for more economies after 1820.[2] As such, we can estimate global output around pandemic episodes. For these reasons, we consider the dynamics of global output growth before, during and after the pandemics of 1831-33, 1898-1900, 1918-19, 1957-58 and 1968-69.[3]

Figure 1 presents average global growth rates before, during and after the five identified influenza pandemic episodes. Several observations are in order. First, in most cases, average global output growth slowed during pandemics relative to before them, as in the case of 1889-90, 1918-19 and 1957-58. Based on these episodes, global output growth dropped by 1.1 per cent. The severity of the slowdowns corresponds to the number of reported and estimated deaths like in the case of the Spanish flu pandemic of 1918-19. Second, global growth after pandemics appears lower compared to before the pandemic, as in the case of the 1889-90, 1918-19 and 1957-58 pandemics. Specifically, global growth was 0.2 per cent lower in the post-pandemic periods compared to before. These stylised facts, however, must consider that the underlying data are estimated, and that the sample contains economies with varying starting dates. For the 1831-33 pandemic, the sample includes 11 economies such as France, the United Kingdom and the United States. In contrast, for 1918-19, the sample includes 36 economies. China is included only in the 1957-58 and 1968-69 pandemics.[4] Moreover, there are other factors driving growth dynamics around and during pandemics. In 1918-19, World War I was in its final stages, while the 1957-58 pandemic coincided with the US recession. Though there are shortcomings, these stylised facts highlight two important points. First, global output growth slows during pandemics; and second, global output growth tends to be slower during post-pandemic years.

Notes: Growth rates (year-on-year, percent) refer to the weighted average growth of individual economies with available estimated Maddison GDP data. Pre- and post-pandemic global growth rates are computed as the average global growth rates two (or three) years before and after a pandemic episode. For instance, pre-pandemic growth rates in 1918-19 are those for 1916-17, while post-pandemic growth rate are those for 1920-21.

Source: Author’s estimates.

But this time, it is different. The world has significantly changed from the late 20th up to the 21st century. Globalisation has taken hold. The movement of people is now faster and, hence, pathogen transmissions are wider and faster. The production of goods and services as well as finance have become global. These facts imply that economic spillovers and disruptions in global value chains may make the economic fallout more severe. Yet advances in science, technology and medicine enabled early information-sharing and made detection possible. Treatment has improved by using ventilators, and vaccines may come sooner than later. Information and communication technology enable people to work remotely. On balance, in this current pandemic, there are growth-supporting factors that may mitigate severe economic fallout. Even under a prolonged pandemic scenario, globalisation and advances in science and technology may, in fact, facilitate a swift transition into new modes of production, delivery and labour market mechanisms.

Nonetheless, output drops and a slower recovery must be avoided, but public health must remain the top priority. An early lifting of restrictions and quarantines, coupled with lax testing, social distancing and contact tracing following the lifting of restrictions, may run the risk of protracted transmission, which may enable the virus to mutate and cause a second wave of pandemic as in the case of the 1918-19 pandemic. To cushion the economic fallout, fiscal policy must play a dominant role. This may take the form of loan guarantees, equity stakes and wider and enhanced social safety nets focusing on small to medium enterprises, lower income groups and the unemployed. Given that half of the world economies (including emerging and developing economies) have general government debt of less than 55 per cent of GDP; as well as the pandemic nature of the economic slowdown, there is scope for these economies to use targeted and effective fiscal policy measures to cushion the economic impact of the pandemic and rump-up the capacity of their respective health care system in dealing with future epidemics and pandemics. Now is not the time for fiscal restraint and debt considerations.

[1] The focus on this blog article is influenza pandemics, which is the same as the current COVID-19 pandemic (Potter (2001)).

[2] Refer to Maddison Historical Statistics of Groningen Growth and Development Centre of the University of Groningen.

[3] Global output based on Maddison Historical Statistics were computed as the weighted average of estimated real GDP, using population as weights. These episodes are considered severe cases conditional on an estimated number of deaths of at least 1 million people.

[4] Based on the five pandemic episodes, excluding China, average annual global growth during pandemics drops by 0.6 per cent from the pre-pandemic average growth rate, while the post-pandemic growth rate slows by 0.1 per cent compared to the pre-pandemic growth rate.

Rogelio is a Senior Economist in the Macroeconomic and Monetary Policy Management pillar at the SEACEN Centre.