- Predominance of the US dollar (USD) funding market, notably post Great Financial Crisis (GFC), has reinforced the macro financial linkages between global financial conditions and capital flows to emerging markets (EM).

- A stronger dollar is linked to tighter global financial conditions and higher tail risk for EM capital flow withdrawal – the financial risk transmission channel.

- The shift to market-based finance via less regulated non-bank financial institutions in capital flow intermediation chains makes policymaking more complex.

- Policies that try and take the tail risk out, build resilience and provide flexibility in the use of a broader set of toolkits, are likely be more effective in a rapidly evolving landscape.

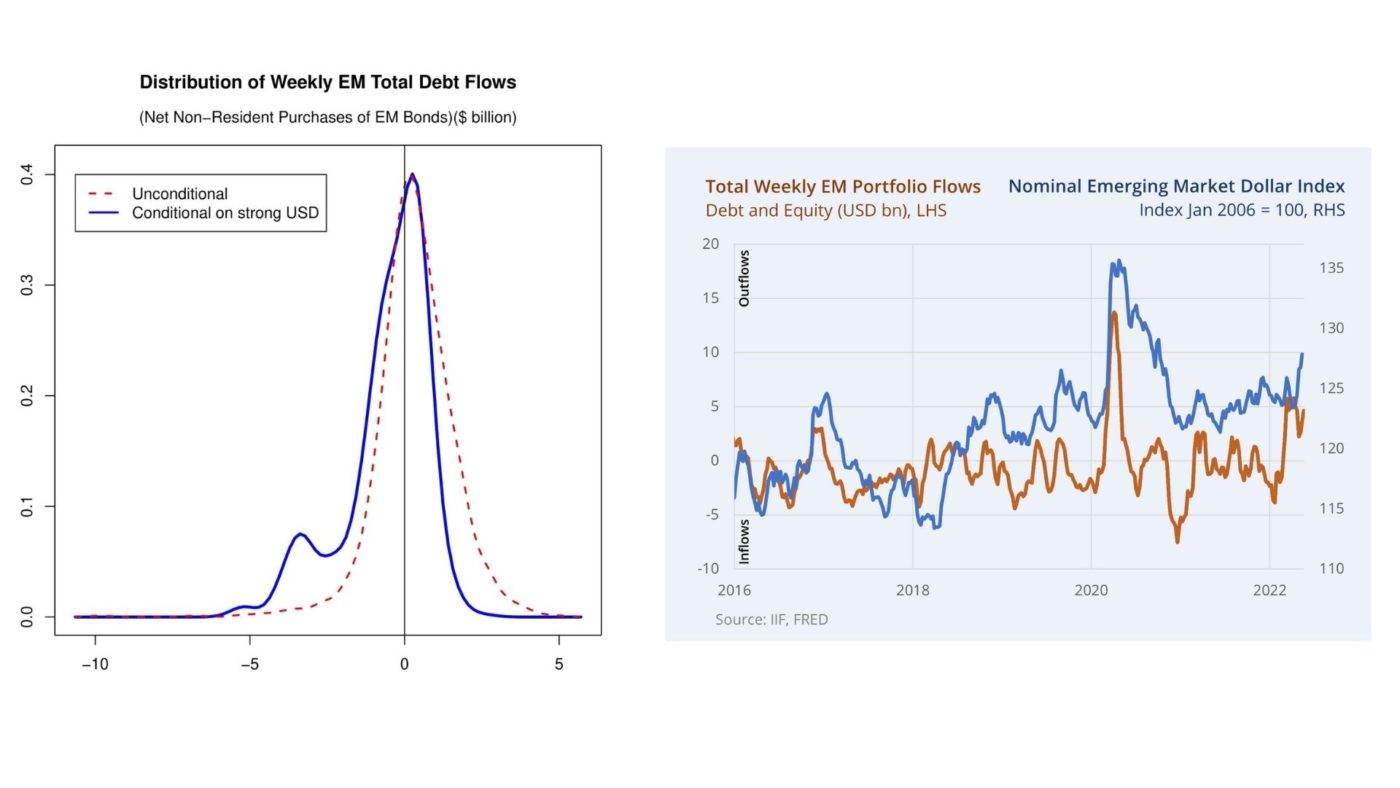

Graph 1: Distribution of Weekly EM Total Debt Flows, Total Weekly EM Portfolio Flows and Nominal Emerging Market Dollar Index

US dollar remains a dominant global funding currency and a source of macro-financial vulnerability for emerging markets. The common thread of the dominance of the dollar in the international financial markets as a funding currency and its movements being a barometer of global risk appetite is playing out under the current narrative of higher interest rate and high inflation. The resultant USD strength is translating into increased stress in EM financial conditions with EM risk premia rising and having implications for macro-financial stability of EM economies.

Graph 2: US Dollar-Denominated Credit to Non-Banks and Foreign Currency Credit to Selected Emerging Market and Development Economies (EMDEs)

The narrative of the post GFC period of high global liquidity, driven by very low interest rates and quantitative easing (QE) by advanced economies, is now being played in reverse. Global financial conditions are tightening, buffeted by another supply shock (commodity shock partly driven by the war in Ukraine, zero COVID-19 policy related lockdowns in China) combined with demand-supply imbalances and high inflation, prompting rising US interest rates and the talk of quantitative tightening (QT). High inflation, slowing global growth and accelerated monetary tightening are all weighing on the outlook for EMs.

The post GFC narrative of ample global liquidity set the stage for EM capital flows becoming even more sensitive to changes in global financial conditions. On the EM borrower side, it was easier to access financing in the dollar market during periods of low US interest rates and dollar weakness while most EMs are reliant on foreign inflows to finance their fiscal and current account deficits. As a result, US Dollar liabilities of EMs, notably in fast growing Asia, rose since the GFC. Many EM Asia economies have significant debt denominated in foreign currencies — of which the US dollar plays a dominant role (Park et al. (2020)). On the creditor side, institutional investors from advanced economies invested in EM local currency sovereign bonds, looking for higher yields and potential returns from the exchange rate exposure. The increased foreign participation in local currency bond markets increased the sensitivity of such yields to global conditions that dictate foreign portfolio investor sentiment.

An important difference was a notable shift from bank loans to portfolio debt instruments of EM financial institutions and non-financial corporates. The shifting of risk to less regulated non-bank financial institutions amplified the vulnerabilities to tail events from currency mismatches, both for the EM issuers in foreign currency and advanced economy (AE) investors in local currency. These vulnerabilities are compounded by regulatory and supervisory challenges faced by the less regulated non-bank financial institutions (NBFIs) as these played a key role in funding EM external debt post GFC, as AE investment funds assets tripled since GFC. While this provided more diversified funding for EMs, they became more susceptible to the changes in global financial conditions and investor sentiment.

The buildup of the post GFC macro-financial vulnerabilities was put through the stress test during the COVID-19 shock. EMs saw significant asset price declines from large scale non-resident outflows resulting in depreciation pressures and higher volatility on EM currencies that needed massive policy support. Economies with high foreign exchange (FX) debt relative to reserves tended to suffer larger debt outflows. During the COVID-19 shock EM investment funds experienced large redemptions, larger than during the ‘taper tantrum’ shock, while funds holding illiquid assets were hit harder.

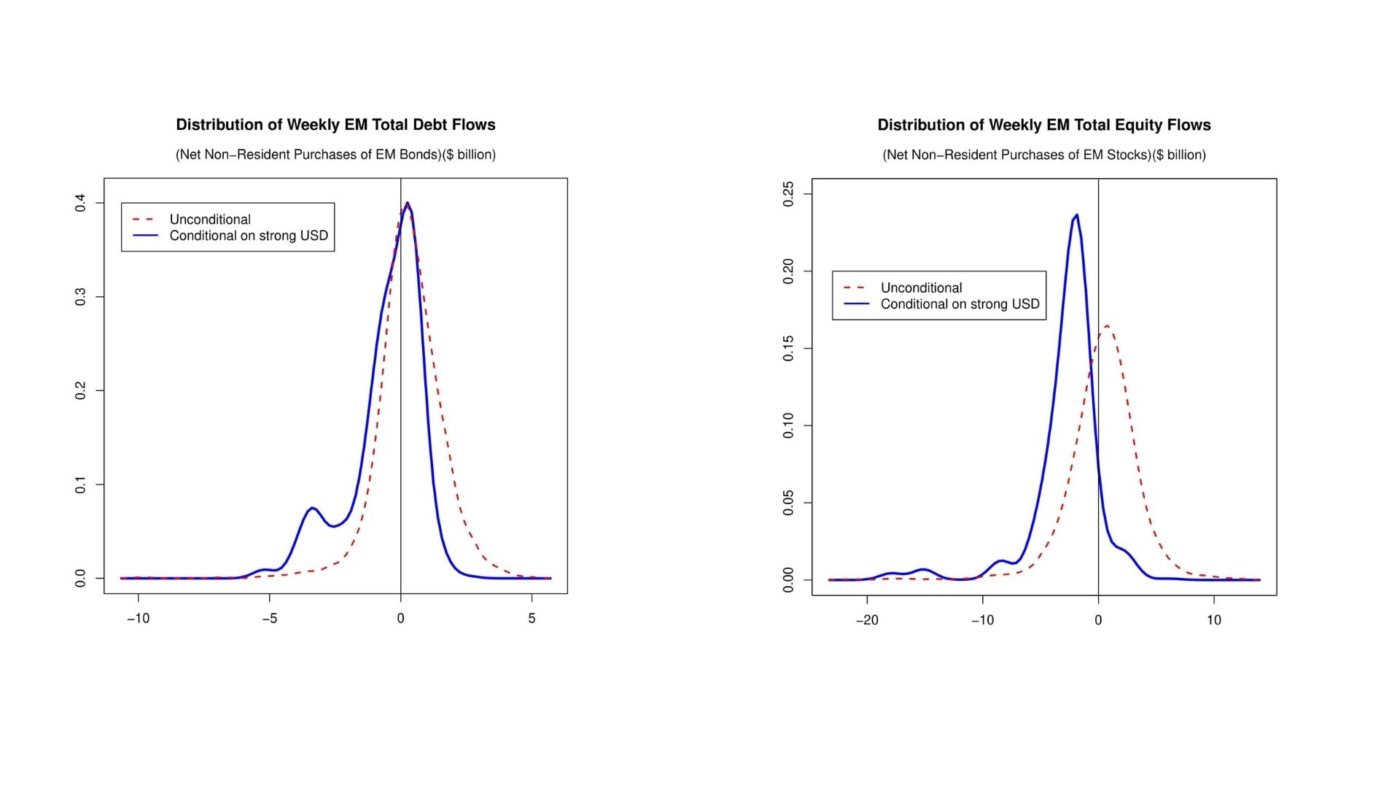

The current episode of capital outflows, driven partly by the appreciation of the dollar, is another stress test for EMs. Empirical evidence shows that US dollar appreciation is associated with worse economic performance for emerging market economies (Hofmann and Park (2020)). A related phenomenon also plays out with regards to capital flows. Since 2006, total capital flows to EMs, be it portfolio debt flows or portfolio equity flows, can be subject to higher tail risks when the US dollar rises strongly against a weighted basket of domestic EM currencies (Graph 3).[1] A stronger USD is associated with a higher likelihood of reduced EM bonds (left-panel) and stocks (right-panel) flows (compare the blue distribution of flows conditioned on strong USD to the red distribution which is the unconditional distribution of net non-resident portfolio flows).

Graph 3: Distribution of Weekly EM Total Debt and Equity Flows

How does this risk transmission work? Given the role of the US dollar as a global funding currency, a stronger dollar leads to a tightening of global financial conditions. A higher dollar is perceived as an indicator for risk aversion and a flight to safety. As investors turn to ‘risk-off’ mode, they retreat from EM financial markets. Lower global liquidity, mainly through the shortage of dollar credits and non-resident portfolio capital outflows put further pressure on EM exchange rates.

The impact is more significant for EM borrowers with balance sheet mismatches on FX and liquidity. Balance sheets of corporates, financial institutions and households with net FX liabilities are negatively impacted with the valuation of their net worth declining. Funding long-term local currency assets with short-term dollar liabilities compound FX mismatches with liquidity amplifiers. Financial institutions in EMs (especially with current account deficits) that tend to fund in the US dollar market become more risk averse on their lending portfolio (values-at-risk (VaRs) indicate lower risk tolerance). Corporates with higher FX exposures also cut down on their investments. The resultant slowdown of the flow of credit to the economy, in turn, hurts growth.

As for advanced economy creditors who have invested cross-border in EM local currency denominated assets, an appreciation of the dollar translates to higher losses on their portfolios as most tend to invest unhedged. Hedging their local currency (LC) exposures in imperfect financial markets and with market liquidity drying up during stress periods can force them to liquidate, putting further pressure on EM assets. Therefore, a stronger dollar is associated with net outflows from global bond funds with EM investments or dedicated EM bond funds and the like.

Policy Implications

More granular and higher frequency capital flow data, notably on portfolio flows, provide policymakers and market analysts a better opportunity to understand the dynamics and efficacies of capital flows. New methodologies to analyse these data is shedding more light on the time-varying risks. As a result, policy analysis and measures can go beyond looking at the medians of the distribution and focus on the tails, especially during stress times. Using median expectations for policymaking may lead to underestimation of the risk.

Policies need to take out the tail risk (and shift the distribution to the right), by building buffers and resilience. Policies may have to be preemptive to prevent the snowballing effect of capital outflows. Therefore, evolving policy frameworks should be more holistic by putting more weight on exchange rate and capital flow stabilization. Foreign Exchange intervention (FXI) in imperfect markets to manage exchange rate amplification from financial imbalances can be an important policy instrument while having reserve buffers can strengthen the resilience under stress. The effectiveness of FXI can be increased by the presence of capital flow management measures (CFMs) as part of the broader toolkit because systemic risk often build-up in tandem with increasing cross-border interconnectedness and spillovers. All this underlies efforts to form an integrated perspective on monetary policy, macroprudential policy, capital flow measures and foreign exchange intervention.

[1] The graph presented above uses high frequency Institute of International Finance (IIF) data on non-resident portfolio capital flows and the broad US dollar index. Unconditional and conditional densities of net non-resident portfolio EM flows during the period from 6 January 2006 – 6 May 2022. Strong USD is defined as at least a 5 per cent appreciation of the USD index in each week. This corresponds to the extent of US dollar appreciation during the first half of 2020. Non-resident net portfolio debt and equity flows refer to one week-ahead outcomes after the appreciation. The densities are estimated using a kernel density estimator with an Epanechnikov kernel function.