This blog post is based on the policy roundtable held on 15 May 2026, featuring panellists Professor Danny Quah, Professor Shang-Jin Wei, Professor Joseph Cherian, and Associate Professor Jamie Cross.

In the age of geoeconomics, major economies increasingly use their power, market influence, and cross-border interdependence to advance national and strategic goals. Tariffs, sanctions, export controls, and market-access restrictions are now common policy tools. As a result, access to capital, energy, technology, and global trade and financial networks can no longer be assumed and are increasingly shaped by geopolitical alignment.

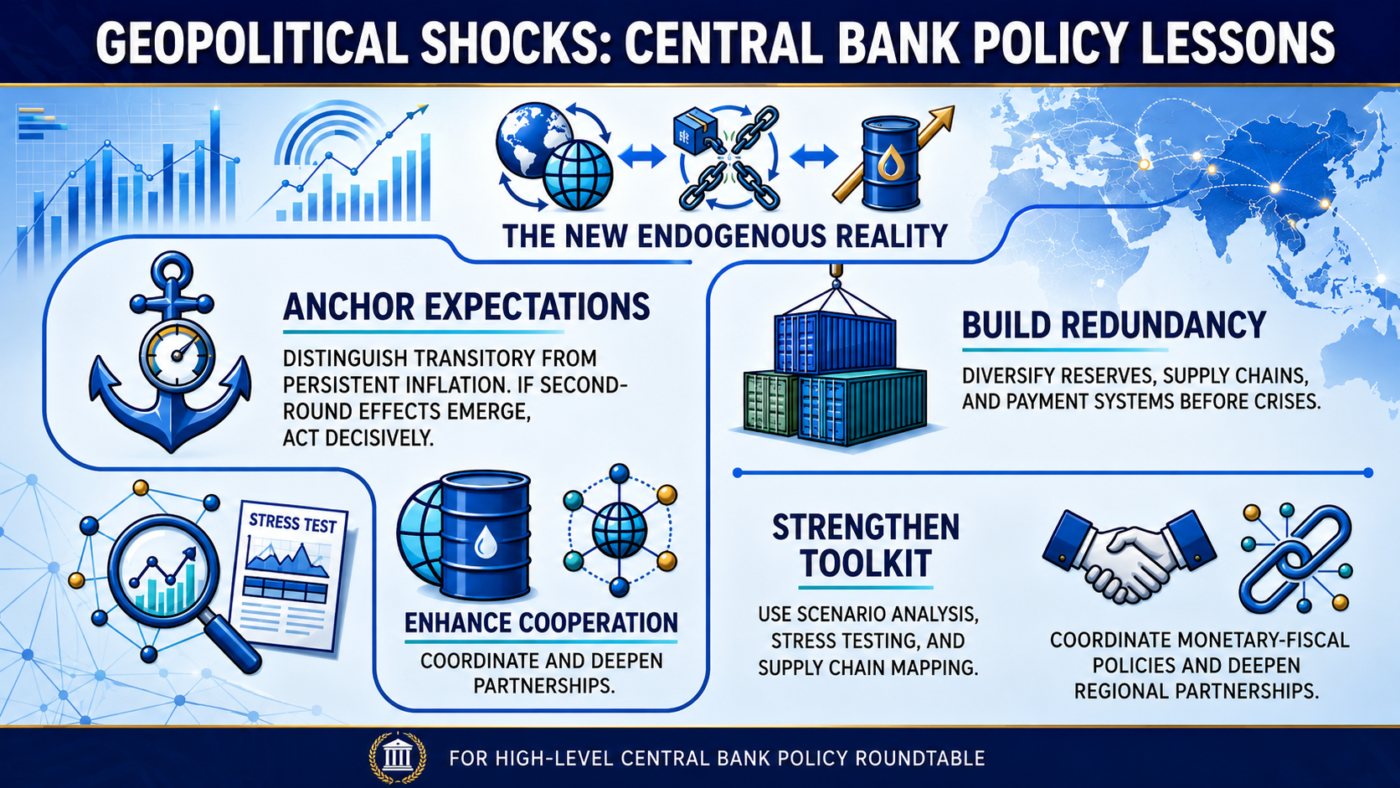

Against this backdrop, war-related oil shocks, trade restrictions, geopolitical uncertainty, and shifts in the global monetary and financial system can no longer be treated as exogenous, isolated shocks. Rather, they are endogenous and mutually reinforcing, interacting through energy prices, supply chains, exchange rates, financial markets, fiscal positions, and expectations. For central banks, resilience must therefore extend beyond narrow price stability considerations to encompass anchoring inflation expectations, sound external liquidity management, efficient payment systems, well-functioning markets, strong data and modelling capacity, and robust regional cooperation.

Oil shocks are particularly challenging because they involve both a relative price increase and broader second-round effects. The initial impact is a rise in energy costs, which will feed into transport, production, electricity generation, and household fuel consumption. Higher oil prices also pass through to food, plastics, fertilisers, logistics, and a wide range of intermediate goods. These second-round effects can generate broader inflationary pressures by pushing up consumer and business expectations, potentially triggering a wage–price spiral. Central banks must therefore distinguish carefully between a temporary supply shock and a more persistent inflation process that could de-anchor inflation expectations.

The standard view among central banks is that monetary policy should look through a transitory supply shock when there is no evidence of second-round effects. However, this approach may not be optimal when second-round effects are evident. Central banks can bring inflation closer to the target with a corresponding policy response by pre-emptively raising interest rates to curb demand and help manage second-round effects.

However, while higher interest rates can dampen demand and contain these effects, they cannot increase oil supply, reopen shipping routes, clear conflict-related disruptions, restore insurance coverage, or diversify supply chains in the face of prolonged war. This creates a difficult trade-off. If central banks tighten too aggressively, they risk deepening the decline in output without addressing the underlying supply constraints. If they respond too weakly, the shock may become embedded in wages, prices, and expectations. The key lesson is that central banks need a clear reaction function: when credibility is strong, they can accommodate the temporary first-round effects of a shock, but they must act decisively if second-round inflationary pressures begin to emerge.

The fiscal–monetary interface becomes more critical in this context. Governments typically respond to energy shocks through subsidies, tax relief, administered prices, or transfers to households and firms. While these measures can ease immediate welfare costs, they also carry risks. Broad subsidies are expensive, often poorly targeted, and may delay necessary adjustments to new relative prices. In Southeast Asia, where energy and food subsidies are politically sensitive, prolonged subsidy programmes can weaken public finances and create future fiscal pressures on pensions and social spending. At the same time, high public debt can expose central banks to the risk of fiscal dominance, especially when they need to consider raising interest rates to curb inflation. Central banks should therefore clearly communicate the macroeconomic trade-offs: targeted, temporary, and transparent fiscal measures are less inflationary and less damaging to public finances than open-ended price suppression.

Another lesson from the policy roundtable is that central banks need to treat geopolitical shocks as endogenous and strategic, rather than exogenous and isolated. Traditional macroeconomic models often define shocks as unexpected, external, and statistically identifiable innovations. But sanctions, trade restrictions, blockades, and conflict-related disruptions are policy choices made by strategic considerations. They may be designed to harm particular economies or to change incentives. This creates a modelling challenge. Central banks need tools that can handle nonlinearity, tail risks, scenario dependence, and interaction across shocks. Standard VARs, linear forecasting models, and historical correlations remain useful, but they are not enough. Scenario analysis, stress testing, network models, supply-chain mapping, and narrative-based risk analysis should become part of the macro-policy toolkit.

For small states, the panel’s message was that shocks should not be analysed in isolation. Countries may face a “China shock,” a “US shock,” weakening multilateralism, climate stress, and energy-market disruptions simultaneously. While economic theory suggests one instrument per shock, small states lack that degree of policy capacity. Monetary and fiscal policy, reserves, prudential tools, and exchange-rate management must therefore operate under tight institutional, political, and balance-sheet constraints. This calls for a broad-spectrum approach to policy analysis: central banks should assess how trade, energy, financial, and geopolitical shocks interact, rather than relying on separate assessments that overlook compounded risks.

Diversification was another central theme. Dependence on a single dominant market, currency, payment infrastructure, supplier, insurer, or security provider creates concentrated vulnerability. Diversification does not mean retreating from globalisation. It means avoiding fragile single points of failure. For central banks, this has direct relevance to reserve management, payment systems, foreign-exchange liquidity arrangements, correspondent banking channels, and financial-market infrastructure. The lesson is to build redundancy before crisis conditions appear. Once shipping lanes close, insurance markets seize up, or dollar liquidity tightens, diversification becomes much more expensive.

The discussion of capital markets pointed to a broader financial stability concern. War, oil shocks, and trade restrictions can simultaneously raise geopolitical, monetary policy, fiscal policy, and sovereign debt risks. These risks affect exchange rates, repo markets, bond markets, equity prices, and insurance markets. For Asian economies that rely heavily on the US dollar for international trade and finance, dollar liquidity remains a core vulnerability. Central banks, therefore, need to monitor not only domestic credit conditions but also offshore dollar funding, FX swap markets, repo-market functioning, sovereign spreads, and the availability of trade and shipping insurance.

Payment connectivity is a practical area where central banks can contribute. Lower-cost and more reliable regional payment systems can support intra-regional trade, reduce transaction frictions, and make regional economic links more resilient. This is not a substitute for macroeconomic adjustment, but it is a concrete institutional contribution. Cross-border payment connectivity, local-currency settlement arrangements, and regional liquidity facilities can reduce dependence on a narrow set of external financial channels. Central banks are also major participants in FX swap markets, so their role in liquidity backstops and market confidence is not peripheral.

The panel also suggested that multipolarity should be treated as an operational reality rather than an ideological position. Geoeconomic fragmentation is increasingly becoming a structural feature of the global economy. If the world is no longer organised around a stable unipolar provider of security, liquidity, insurance, and market access, then small open economies need to adapt. This does not imply abandoning existing partnerships. It means building capacity to operate in a world where no single external anchor can be assumed to provide full insurance. For central banks, that means reserve diversification, deeper regional cooperation, stronger contingency planning, and better understanding of how geoeconomic and financial fragmentation affects trade invoicing, capital flows, and exchange-rate dynamics.

The outlook is not entirely bleak; every crisis also creates structural opportunities. Energy shocks and trade restrictions may accelerate investment in renewables, regional supply chains, electric vehicles, semiconductors, and strategic reserves. Central banks are not responsible for industrial policy, but they must understand how structural shifts affect inflation, external balances, productivity, credit allocation, and financial stability. Green technology, energy security, and supply-chain reconfiguration will alter relative prices and investment patterns. These changes should be incorporated into medium-term forecasts and financial stability assessments.

The final lesson is institutional resilience. The Governor of Bank Negara Malaysia’s point about resilience against repetitive stress is central. These shocks are unlikely to be one-off events. Central banks need systems that can withstand repeated stress rather than frameworks designed around a return to normal after each disruption. That means improving data infrastructure, scenario design, market intelligence, communication, coordination with fiscal and regulatory authorities, and regional policy networks. The aim is not to forecast every shock precisely. It is to build enough analytical and institutional capacity to respond coherently when shocks arrive in clusters.