This blog is based on a presentation made by Ceyhun Elgin at the SEACEN online course “Practical use of AI in monetary policy” on 28-30 April 2026.

The Falling Cost of Cognition: Why Central Banks Must Rethink the AI Shock

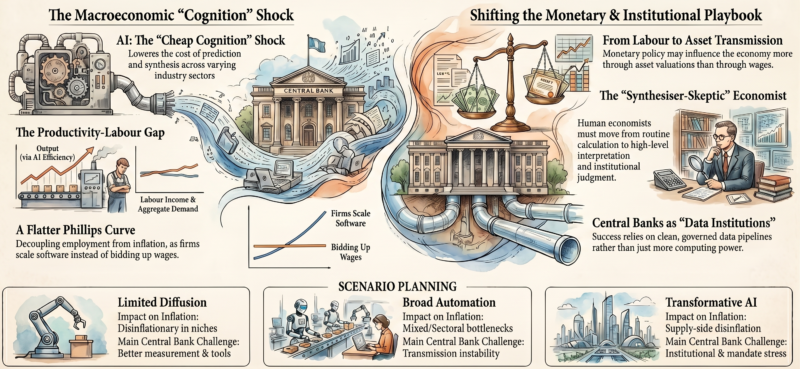

Artificial Intelligence (AI) is often discussed as a futuristic marvel or a tool for specialised automation. However, for central bankers and macroeconomists, it represents something far more profound: a fundamental macroeconomic shock. According to Professor Ceyhun Elgin, the most practical way to define AI is as a family of technologies that dramatically lower the marginal cost of “economically useful cognition”, including prediction, search, synthesis, and decision support.

When the cost of intelligence falls, and its scalability rises, the basic assumptions underlying monetary policy frameworks begin to shift. Central banks cannot afford to wait for certainty before acting.

AI as a “Total System” Shock

Most economic shocks that central banks care about are isolated. For example, a commodity price spike raises costs; a fiscal stimulus moves demand. AI is different because it can create simultaneous shocks. It can disrupt production, labour markets, commodity pricing, data generation, and communication all at the same time.

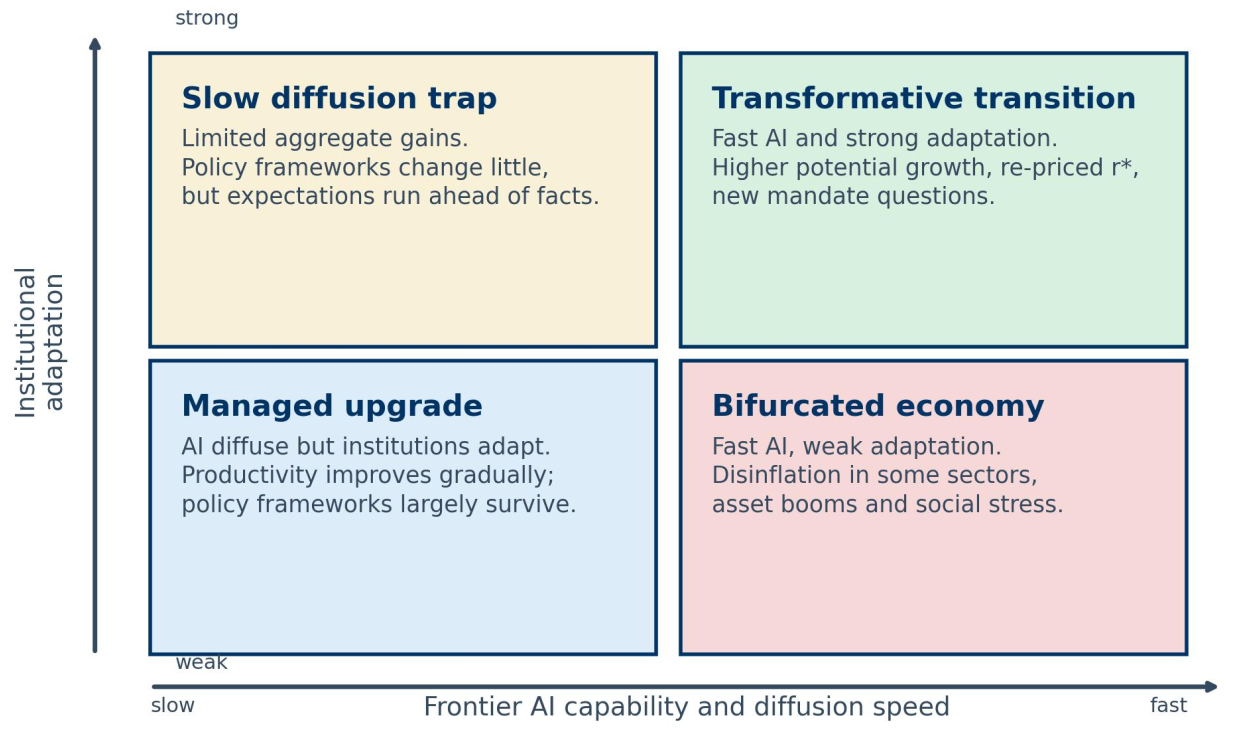

Figure 1: Four AI-Macro Worlds for Central Banks

Because the future of AI is wrapped in “radical uncertainty,” central banks should operate through scenario discipline rather than single forecasts. As illustrated by Figure 1, three primary paths are highly possible:

- Limited Diffusion: Productivity improves slowly; current models remain usable with minor updates.

- Broad Automation: Adoption is significant but uneven across the different sectors, leading to unstable policy transmission and sectoral bottlenecks.

- Transformative AI: Cognition becomes abundant, requiring a fundamental revision of macroeconomic relationships and potentially leading to powerful supply-side disinflation.

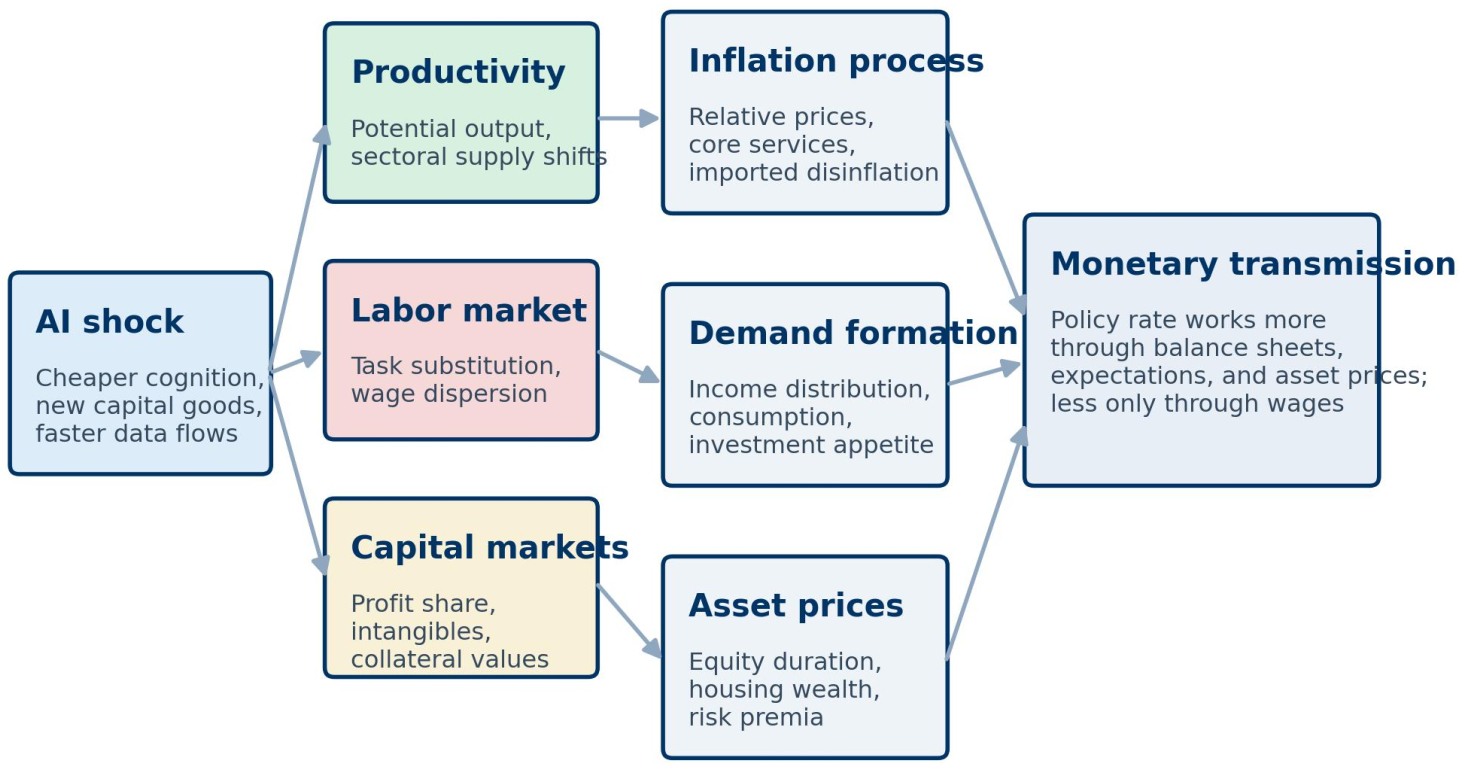

The Shifting Transmission of Monetary Policy

Traditionally, monetary policy works primarily through the labour income channel: interest rates affect demand, which in turn affects labour markets and wages, eventually shaping consumption and inflation. In an AI-intensive world, this chain may weaken.

If firms respond to demand not by hiring more people, but by scaling software and automation, the labour market may lose its role as the primary driver of inflation. Instead, transmission may shift toward asset valuations and balance sheets. As productivity gains are captured by capital owners, demand formation will depend increasingly on wealth effects and collateral values rather than steady wage growth (See Figure 2).

Figure 2: How the Transmission Mechanism May Shift in an AI-intensive Economy

This also complicates the behaviour of the neutral rate of interest (R*). While a productivity boom could push R* higher by creating new investment opportunities, the risk of “concentrated gains”, where winners save more than losers spend, could actually exert downward pressure on the R*.

The New Labour and Inflation Puzzle

With changing dynamics between the labour market and inflation, the relationship between unemployment and inflation, as represented by the Phillips Curve, is likely to become flatter or more unstable. In an environment where cognitive tasks are easily automated, labour market tightness may no longer map into wage pressure as clearly as before. Firms may simply scale software rather than bidding up wages for human workers.

Furthermore, while AI is generally disinflationary by lowering service and back-office costs, it may create new inflationary bottlenecks in areas like electricity, specialised chips, and cloud capacity. This creates a complex price environment where some sectors experience rapid deflation while others face significant cost spikes.

Institutional Challenges: Data and Communication

For central banks as institutions, AI represents an informational democratisation. When every market participant has access to AI tools that can parse speeches and detect internal inconsistencies instantly, the central bank loses its analytical monopoly. Narrative discipline becomes critical; any lack of coherence in communication will be identified and traded upon in seconds.

To survive this era, central banks must transition from being model institutions to data institutions. The marginal value of a clever new model is often lower than the value of a clean, fast, and well-governed data pipeline. Alternative data, from payment systems to web signals, will be essential to monitor an economy that is changing faster than official statistics can capture.

The Human Element: Scepticism and Judgment

Does AI make the human economist obsolete? On the contrary, it raises the bar for human judgment. While AI can handle data cleaning, coding, and first drafts, it cannot navigate the political economy of distributional conflict or frame complex policy trade-offs.

As routine analysis becomes commodified, the competitive advantage of the central bank economist will lie in synthesis, scepticism, and the ability to interpret uncertainty. Junior economists must be trained not just as calculators, but as policy translators who understand why certain indicators matter beyond the raw numbers.

Conclusion: Preparing for the AI Revolution

The challenge for central banks is not simply to use AI, but to understand how AI changes the economy they must respond to. This requires a proactive agenda:

- Building explicit AI scenarios into regular policy discussions.

- Investing in alternative data pipelines to track shifts in real-time.

- Strengthening data governance as a core policy function.

- Redesigning workflows and workforce planning before technology forces the change.

Ultimately, the future of monetary policy in the age of AI depends less on the power of the algorithms and more on the adaptability of our institutions and the quality of our collective judgment.