As emphasised in opening remarks by Deputy Governor Jessica Chew at the Central Bank Payments Conference on 11 June 2024 in Kuala Lumpur, “The payment system lies at the heart of economic activity. If money is the lifeblood of the economy, then payment systems represent the veins that allow money to flow to where it is needed.”

Central banks’ mandates on payment systems worldwide are diverse, encompassing the promotion of stability, efficiency, and security. These mandates also include a “catalytic role”[1] to drive innovation and progress within the payment ecosystem. Many central banks refer to this role in their publicly available payment strategy documents, including the ECB, Bank Indonesia, Bank Negara Malaysia, Bangko Sentral ng Pilipinas and the De Nederlandsche Bank. This role becomes particularly useful when market outcomes tend to be suboptimal, such as when transaction costs are high, financial inclusion is not ubiquitous, or innovations are not progressing as desired.

During SEACEN in-person payment courses, participants frequently ask about the catalytic role of central banks. Their curiosity and questions have been the inspiration for this blog. It’s fair to say they acted as catalysts themselves!

Understanding suboptimal market outcomes in payments

Understanding payments in a holistic sense is crucial, including how individual elements relate to one another when decoding suboptimality issues.

- High transaction costs

High transaction costs can discourage the use of certain payment methods, reduce overall transaction volumes, and hamper economic activity. These costs may arise from fees charged by payment processors, banks, or intermediaries, which can be highly expensive for both consumers and businesses. A good example is cross-border payments.

- Limited financial inclusion

A significant portion of the population may be excluded from formal financial systems due to various barriers, such as lack of access to banking infrastructure, high service costs, or lack of financial literacy. This exclusion can limit economic opportunities and sustain poverty, as highlighted by the BIS.

- Lack of interoperability

When payment systems do not communicate with each other adequately and smoothly this can create fragmentation, making it difficult for users to transfer funds between different platforms or across borders. This lack of connectivity can hinder the efficiency and reach of payment systems.

- Slow adoption of innovation

If the adoption of new payment technologies and innovations is slow, it can result in outdated systems that do not meet the evolving needs of users. This can stifle economic growth and the development of more efficient and secure payment methods.

- Security and fraud risks

Inadequately secured payment systems can be vulnerable to fraud and cyberattacks, leading to financial losses for users and a lack of trust in the system. This may discourage people from using digital payment methods and limit the growth of the digital economy.

- Lack of transparency

A lack of transparency in payment systems can create information asymmetries where consumers do not fully understand the fees, risks, or terms associated with different payment options. This misunderstanding can lead to suboptimal decision-making and diminished consumer welfare.

- Inadequate regulation

Insufficient or overly restrictive regulation can either fail to protect consumers and ensure fair competition or stifle innovation and the entry of new players into the market. Striking the right balance in regulation is crucial for the healthy development of payment systems.

- Market dominance and reduced competition

When a few players dominate the payment market, it can lead to reduced competition, higher prices, and less innovation. This market concentration can disadvantage smaller players and consumers.

Given these suboptimal market outcomes, the catalytic role of central banks in addressing these inefficiencies becomes increasingly important.

Defining the catalytic role: key objectives for central banks in modern payment systems

The catalytic role for central banks could include, among other responsibilities, the active promotion of innovation, best practices and facilitating the integration of market infrastructures within the payment ecosystem without imposing strict regulations.

Although the integration of market infrastructures is mainly a market-driven process, it may present coordination problems at times and therefore necessitate balancing the diverse interests of various stakeholders in the ecosystem. Central banks then step in and act as catalysts to overcome these challenges, ensuring that payment systems evolve efficiently and inclusively. This approach focuses on fostering an environment conducive to technological advancements and market developments.

Some examples of interventions could include, among others:

- Central banks and regulators can implement policies to lower transaction fees, such as promoting competition among payment service providers or investing in shared payment infrastructure.

- Initiatives to improve financial literacy, expand banking infrastructure, and offer low-cost banking services can help bring more people into the formal financial system.

- Promoting interoperability standards and protocols that ensure different payment systems can work together seamlessly can enhance efficiency and user convenience.

- Regulatory sandboxes and support for fintech startups can stimulate the development and adoption of new payment technologies.

- Implementing strict security standards and conducting regular audits can protect against fraud and cyber threats, thereby building trust in the payment system.

Unpacking the catalytic role: why central banks are perfectly positioned to play this role?

Central banks employ various tools to fulfill their catalytic role, including, among others, presentations, speeches, reports, studies, and press releases, to assess and measure progress towards their objectives in terms of their mandates on payment systems.

They are uniquely positioned to play the catalytic role due to several factors such as:

- Market knowledge

Central banks possess extensive knowledge of the payment market, including its dynamics, trends, and the needs of different participants. That’s why they can easily identify gaps and opportunities by recognising areas where market-driven processes may be delayed or where there are opportunities for improvement.

- Policy decisions

Based on the current and future needs central banks can develop informed policies that address market needs, fostering an environment conducive to innovation and growth.

- Neutral party

Central banks do not have commercial interests in the payment market. Due to this neutrality, they are well positioned to build trust between various stakeholders such as financial institutions, payment service providers, and end-users.

- Mediators

In their catalytic role central banks can act as impartial mediators to resolve conflicts and align the interests of different parties in the payment ecosystem.

- Bringing supply and demand sides together

Central banks can facilitate the collaboration and bring together the main stakeholders in their jurisdictions between the supply side (e.g., financial institutions, payment service providers, fintechs, etc.) and the demand side (e.g., consumers, umbrella organisations and businesses).

They can achieve this by, among others:

- Organising forums and workshops: Creating platforms for dialogue and collaboration where stakeholders can share their perspectives and work towards common goals[2].

- Promoting standardisation: Encouraging the adoption of common standards and protocols to ensure interoperability and efficiency within the payment system.

- Supporting innovation: Providing regulatory sandboxes and other support mechanisms to test and implement innovative payment solutions.

Focusing on and Addressing Coordination Problems

In the integration of market infrastructures, coordination problems can arise for different reasons such as fragmented efforts[3], regulatory hurdles[4], and technological disparities[5].

Central banks can use various strategies to address these coordination problems.

Some examples could include:

- Setting clear guidelines: Establishing clear and consistent regulatory guidelines that promote integration while ensuring security and stability.

- Fostering collaboration: Encouraging stakeholders to collaborate on joint projects and initiatives that benefit the overall payment ecosystem.

- Providing infrastructure support: Investing in or supporting the development of shared infrastructure, such as real-time payment systems and digital identity frameworks.

- Giving directions, defining the general objectives and timelines.

- Persistence in achieving the strategy and influencing the end-result.

For example, the ASEAN Payment Connectivity initiative is a good example aiming at integrating and harmonising payment systems across South Asian nations to promote seamless, secure, and efficient cross-border transactions where central banks are involved.

Another example is how the Bank for International Settlements’ (BIS) Innovation Hubs demonstrate that central banks can act as catalysts on a global scale. These hubs facilitate collaboration among central banks and other stakeholders to explore and develop innovative solutions for payment systems. The BIS Innovation Hub in Singapore, for example, focuses on projects such as central bank digital currencies, digital payment infrastructures, and regulatory technology.

Outside the SEACEN region, the ECB’s TARGET Instant Payment Settlement (TIPS) service serves as another good example of how the ECB utilises its catalytic role to enhance the efficiency of cross-border payments within Europe.

Optimising between the catalytic role and issuing regulations or directives

Optimising between the catalytic role and issuing regulations or directives requires a balanced approach that leverages the strengths of both strategies while addressing their respective limitations.

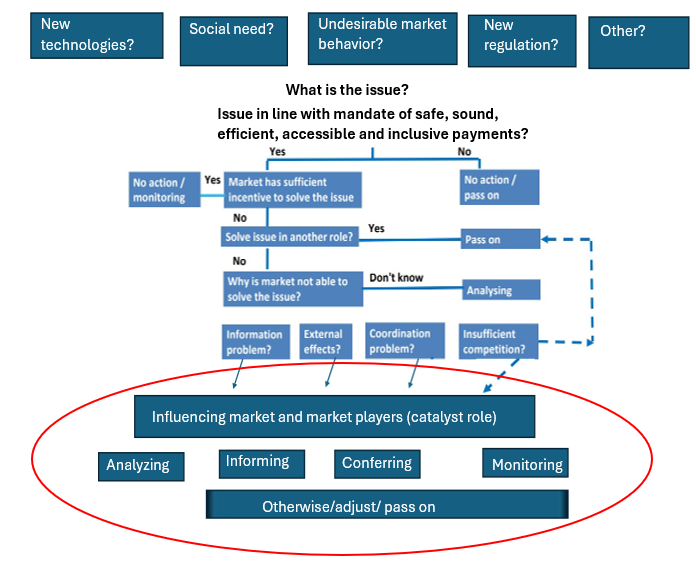

An example of a decision tree to effectively play the catalytic role can be useful when to fulfill the role and be illustrated as follows:

Decision Tree Conditions:

- In line with mandate: Ensuring payments are secure, sound, efficient, and accessible.

- Market inability: Identifying issues that the market cannot solve independently.

- Influence of other roles: Determining if the issue cannot, or can insufficiently, be influenced by other roles.

Considering these conditions, the decision tree might resemble the accompanying diagram. This diagram may serve as a tool to determine when to act as a catalyst and when to pass on issues, ensuring a balanced and effective approach to improving payment systems.

Explanation of Components

- New Technologies? Evaluate whether new technological advancements are driving the issue.

- Social Need? Consider if there is a societal requirement that is not being met by current payment systems.

- Undesirable Market Behavior? Identify if there is any behavior in the market that is not conducive to a healthy payment ecosystem.

- New Regulation? Determine if recent regulatory changes are impacting the payment systems.

- Other? Assess any other factors that might be influencing the payment systems.

- Information Problem? Issues arising from lack of information or misinformation within the market.

- External Effects? Issues stemming from externalities that the market cannot address on its own.

- Coordination Problem? Situations where market participants are unable to coordinate effectively.

- Insufficient Competition? Instances where lack of competition leads to suboptimal outcomes.

Roles in Influencing Market and Market Players:

- Analyzing: Thorough examination of the issue to understand its root causes and implications.

- Informing: Providing necessary information and guidance to market participants.

- Conferring: Collaborating and consulting with stakeholders to find solutions.

- Monitoring: Continuously overseeing the market to ensure compliance and identify emerging issues.

[1] Bank for International Settlements: As catalysts for change, central banks use their influence, knowledge and analytical capabilities, normally in cooperation with other authorities and industry stakeholders, to facilitate the achievement of desired public policy outcomes. This role is less formalised than other functions.

ECB: The Eurosystem acts as a catalyst, especially when the objective is to improve the overall functioning of the euro area market infrastructure, including by means of harmonisation and integration. In this role, the Eurosystem aims to induce, support or speed up market developments by acting as a partner or facilitator, using its technical and analytical expertise and its consultative and cooperative contacts with the private sector, banking supervisors and other public authorities.

[2] Examples include the Dutch National Forum on Payment Systems, the Euro Retail Payments Board and ASEAN Payment Connectivity (here and here).

[3] Different stakeholders pursuing their own interests without a cohesive strategy.

[4] Variations in regulatory frameworks that interfere with seamless integration.

[5] Differences in technological capabilities and adoption rates among market participants.

Ayse Sungur is a Senior Financial Sector Specialist in the Financial Stability, Supervision, and Payments Pillar at the SEACEN Centre.